Welcome back to the weekly “Bitesize Finance” content. This week, it’s all about Venture Capital (VC) and Private Equity (PE), arguably one of the most written about buzzwords particularly if you follow the technology sector. Whilst most people are familiar with Venture Capital (basically the vehicle that funds all your favorite startups; Uber, WeWork, Airbnb), less is known about Private Equity. unless you work in finance.

Today, we’re going to break it down for you, so when your friend, fresh from an MBA says she’s applying to a PE firm in Singapore, you can contribute more than nod along.

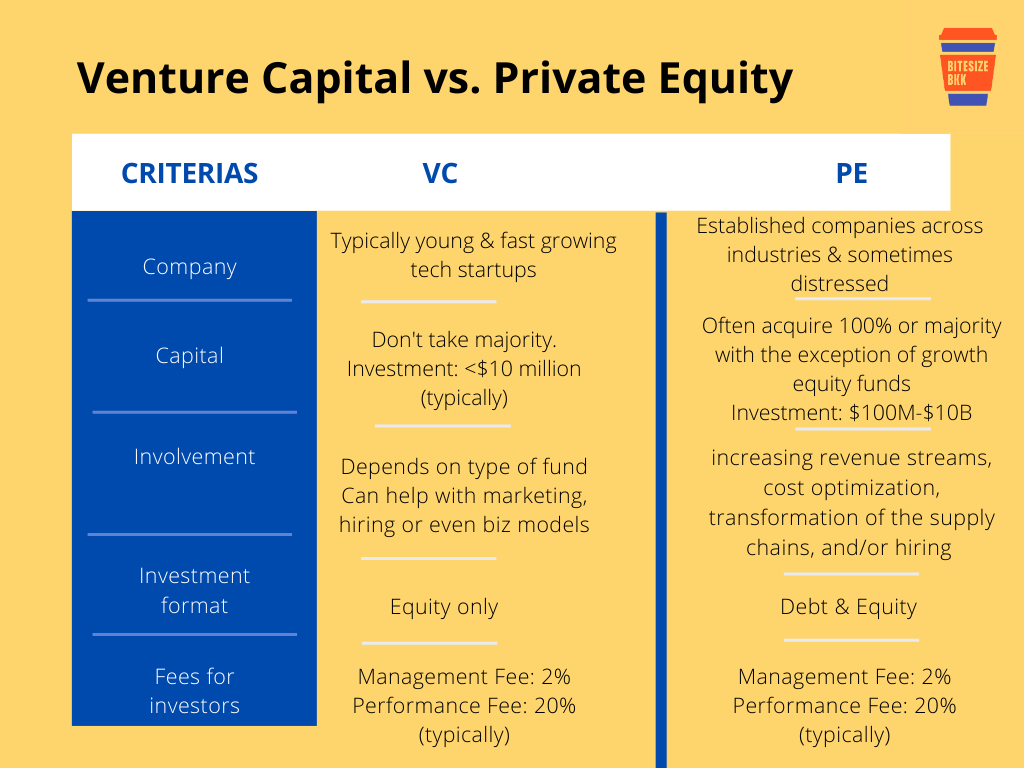

The Similarities & Differences

First off, let’s establish that both VC and PE are part of a complex ecosystem called ‘private markets’. We won’t get into the nitty gritty of it, but companies in private markets do not sell shares to the public and instead give professional investors equity in exchange for funding.

This does not mean that the company won’t eventually file to go public on the NYSE or SET eventually, plenty of high growth startups exit via IPO, as you know.

Both VC and PE firms both raise pools of capital from investors known as limited partners (LPs). The money raised from LPs then is used by the firm to invest in private companies, whether it be a seed stage startup, or a private B2B firm that has been operating for 5 years.

Both VC and PE firms share the same objective most of the time; financial and strategic returns. Both can also eventually sell their stake in a company to another firm, and make a profit.

Here are the key differences

Breaking down the differences

Investment size and involvement are the two big differentiators. For a typical VC investment, they would make smaller, incremental investments in a startup slowly over a span of time, ranging from $1-10M (or lower) for early stage rounds. If the startup grows, they may invest more money to maintain their ownership stake, but it will never be at a majority level like a PE investment. VCs would typically want to get in on a company as early as possible.

A PE firm may spend hundreds of millions to acquire a controlling interest in an established firm, one that doesn’t need help with the initial hiring, marketing or back office work. A PE firm would fix the operational inefficiencies to gear up the company for a sale/IPO.

The culture is somewhat different too. PE firms do extensive market research, often engaging the help of consulting firms, to produce assumption inputs that can be used to build complex financial models on the viability of the target firm. With VCs, although there is some quantitative work, there’s also a lot of relationship building and networking involved, particularly if you’re working for a seed stage/ series A focused fund and scouting for new opportunities.

All in all, the concept and process of a Venture Capital firm is much messier, more often than not, you’re putting money into a charming entrepreneur, a good but unproven idea and not much else.

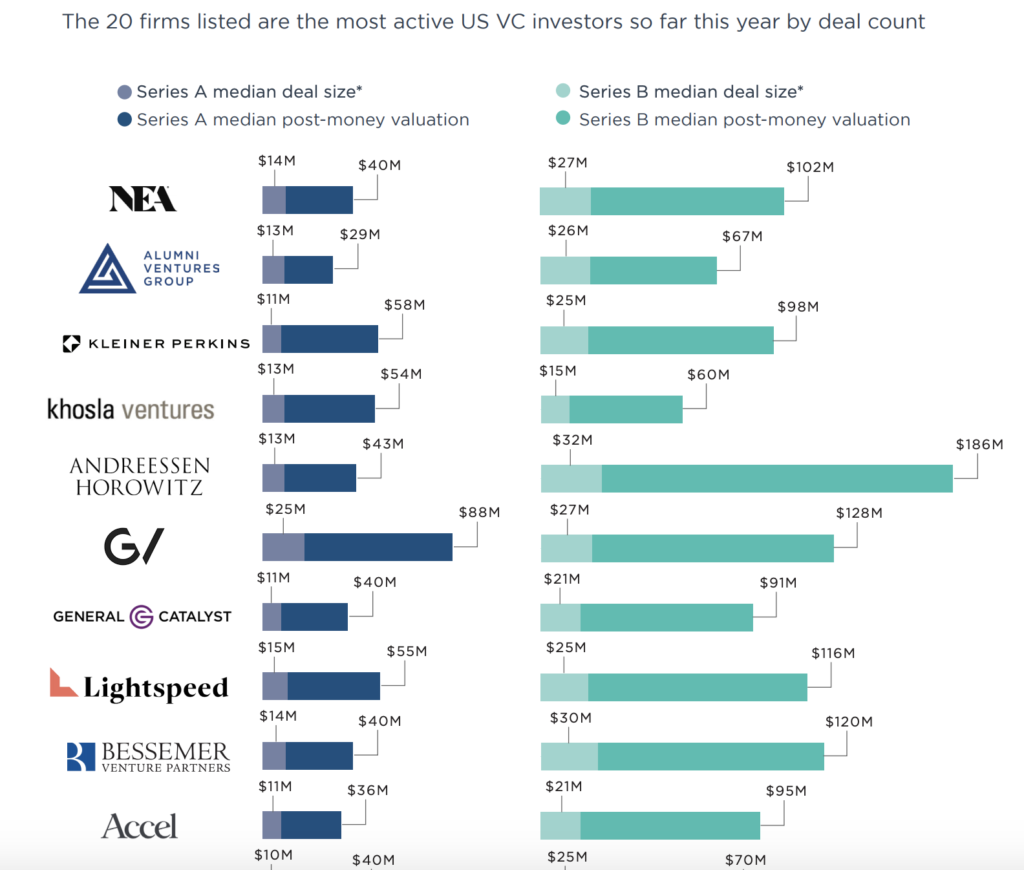

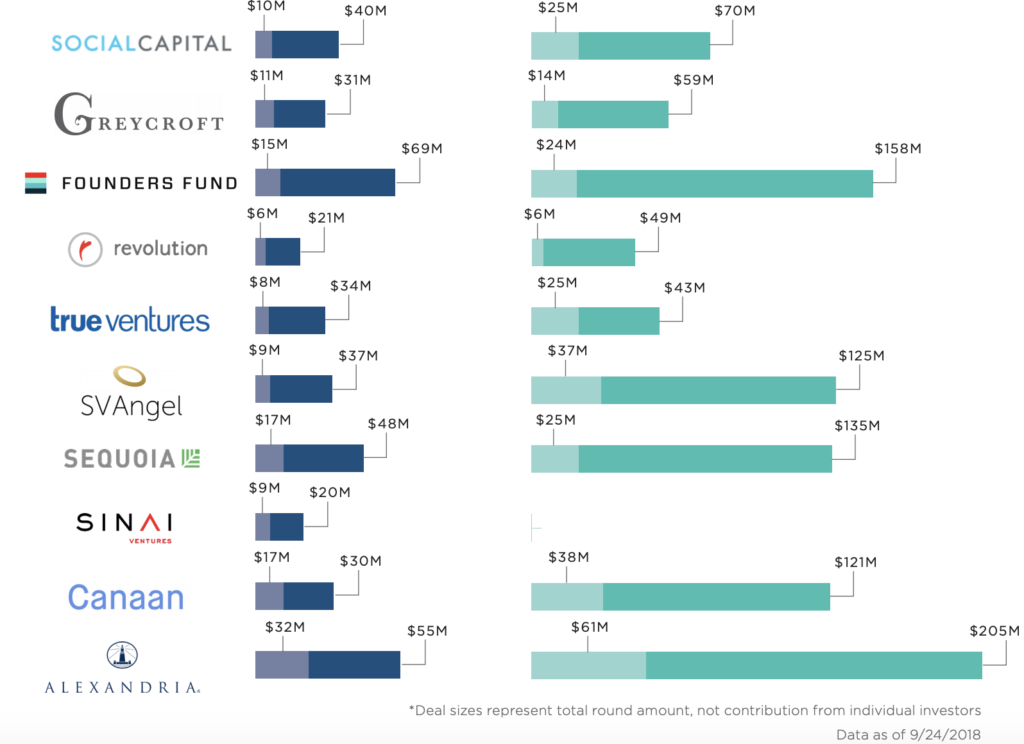

The Global VC Landscape

Source: Pitchbook

Source: Pitchbook

The global Venture Capital landscape has broken records, created trends and propelled growth in otherwise small, unknown companies. We’re talking beyond Facebook and Uber, but also Beyond Meat (plant based meat), Warby Parker (D2C glasses), Monzo (digital bank), Away (suitcases) to sports media startups like The Athletic.

- Around the world, VCs deployed a total of US$251 billion across startups in 2019. In 2019, VCs have invested a total of US$136.5 billion in the US alone.

- There are currently 490 Unicorns in the world. Unicorn is the most overused buzzword in the media, and used when referring to privately valued companies that are worth more than US$1 billion. Interesting fact; when unicorns go public, their valuation can drop (see, mattress startup Casper).

- Not all tech ventures are backed by VCs. In fact, workplace communications platform Basecamp never took Venture Capital money. In fact, its founder Jason Fried is a vocal critic of the ecosystem. “Venture Capital money kills more startups than it helps. Raising more than you need, actually ends up stunting people’s growth as a business”.

- Startups we hear about in the media often raise millions of dollars, and adopt a “growth at all cost” mentality whilst losing millions of investor money in the first few years in order to rapidly grow. This can be difficult to maintain.

Source: CB Insights

The Thai VC Landscape

Source: Techsauce

Thailand’s Venture Capital landscape is quite unique in itself. Our ecosystem is dominated by Corporate Venture Capital (CVC) firms, which means that instead of LPs, the investment fund is owned by a corporate or a bank. This means that investments will typically be strategic focused, for example, a bank owned CVC firm may want to focus on financial technology companies to enhance and compliment its own business.

The objectives and operations are often different to a financial VC firm.

The digital initiatives are often led by corporates and conglomerates in Thailand.

Challenges of VC landscape in Thailand

- In Thailand, one of the main challenges is a lack of exit opportunities, tech companies haven’t made it to the SET. Although, ecommerce enabler aCommerce is gearing up for a public debut, which could inspire some confidence in the ecosystem, although it has not confirmed whether it will be listing on the Singapore Stock Exchange or SET.

- There haven’t been many tech acquisitions in Thailand. Notably, Tencent acquired digital media company Sanook in 2012. Ecommerce marketplace Kaidee was also acquired by a classified solutions provider ESG earlier this year. Technically, Wongnai was acquired by LINE last. month but the company has been around for many years. In Thailand, acquisitions take time.

- There’s not enough money going around in the local tech ecosystem

- Tech adoption and startup solutions are often contained to Bangkok or bigger cities.

- Many consumer facing startups are competing for the same piece of the pie. There are still industries left to be tackled, such as manufacturing, medicine, health (although this is growing) and more. Ecommerce and ecommerce solutions dominate.

- As the landscape is dominated by CVCs, the objectives are very different to that of a financial VC.

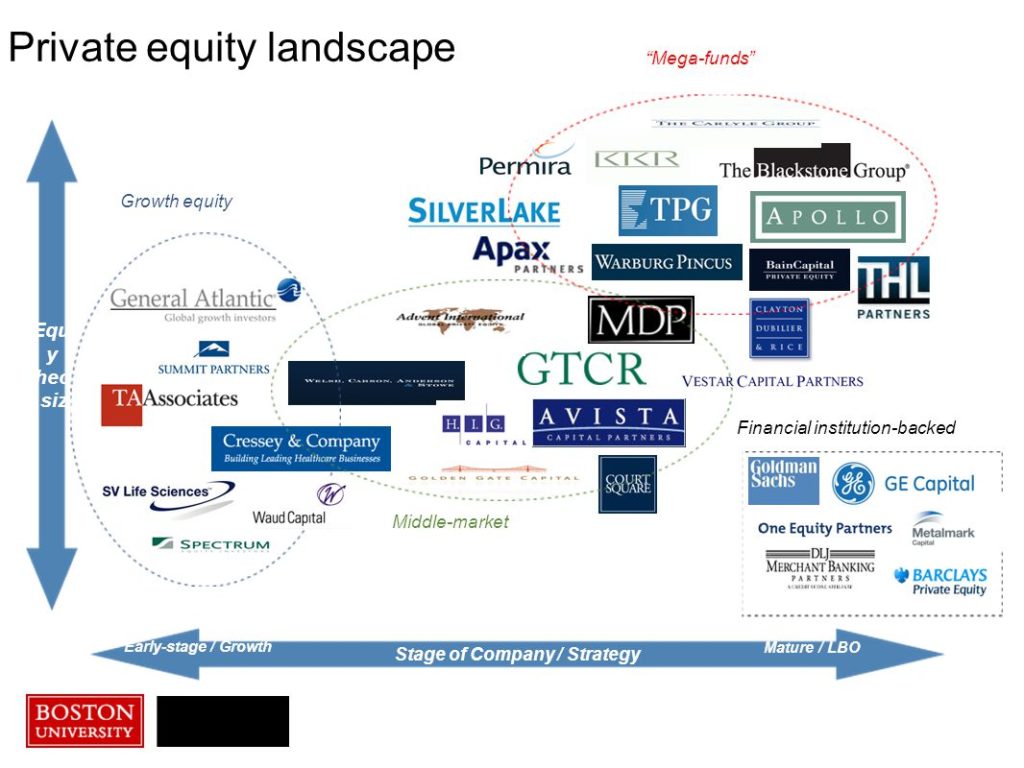

The Global PE Landscape

Private Markets are going mainstream. In fact, Private equity’s net asset value has grown more than sevenfold since 2002, twice as fast as global public equities. Assets under management (AUM) grew by 10% in 2019, and $4 trillion in the past decade. Those are some impressive numbers.

Whilst deal volume has gone through some global decline, one sector is consistent; technology. Just this past year, tech deals accounted for 40% of PE deals in North America.

As of 2019, total AUM for Private Equity totals US$6.5 trillion.

The Local Private Equity Landscape

- Mostly comprises of investors from the region, as there are very few prominent local Private Equity firms in Thailand. The leading firm is Lakeshore Capital with investments in Panpuri wellness and HR software management firm Humanica (now listed on SET).

- Before COVID-19, investors regarded Thailand as a challenging environment for private equity because of the high multiples and a lack of deal opportunities

Post-COVID impact

- Thailand’s PE landscape has been significantly hit by the pandemic, as research by consulting firm L.E.K., which surveyed more than 100 dealmakers – investment bankers, M&A consultants and private equity investors – in Southeast Asia, has shown This is mainly due to sellers being unwilling to bring assets to the market and buyers being concerned about the outlook.

- A lack of available financing amid more lending and investment scrutiny by banks and investors hinders around a quarter of deals currently in process.

- With short-term issues such as liquidity and staffing now mostly tackled, PE funds in Southeast Asia are now switching gears to deal with issues such as resumption of trading and making operating adjustments to the business, with a focus on what lies beyond.

Looking Ahead: Investing Post Pandemic

Venture Capital

When the pandemic hit, most VC firms had to think quick on their feet and navigate the choppy, short term waters. Consumer facing startups in particular, whether it be ride hailing or even ecommerce, had to adjust to either a dramatic drop or surge in demand. VCs focused on either helping portfolio companies survive or deploying emergency cash.

Now, it’s time to establish a long term outlook.

Companies that see an uptick in VC investment will be those that are conducive to the current economic situation, such as digital services, delivery-logistics or communication tools. Whilst people will ultimately return to the way things were, many analysts and investors believe there are some fundamental behavior shifts that will change, leading to the elimination of some businesses and a demand in others.

Fun Fact: Chinese start-ups and technology companies raised more than US$2.5 billion during March, as investors took advantage of lower valuations, hit by the pandemic and seeked out biotech and education startups.

Still, venture capital financing still fell by more than half to US$3.8 billion in Q1 2020, compared to Q1 2019.

Private Equity

For Private Equity firms, the pandemic has seriously tested the industry outlook for 2020 and beyond. Globally, 552 private equity funds reached their final close in the first half of the year, 31% fewer than in the same period last year.

Specific sectors such as technology and healthcare will garner more interest, even for long-term. The bottom line is though, North American continues to dominate the Private Equity ecosystem, despite increased activity in Asia Pacific in H1 2020, due to quicker recovery rate from the pandemic.

Now, the tide is turning back to the US as the market for venture funds skewed heavily toward North America, away from Asia, and toward large funds to probably minimize investment risk.

Ultimately, the VC & PE outlook shares post-pandemic similarities. North America continues to dominate the landscape, and productive, forward facing companies that tackle relevant problems will remain attractive.