For those who didn’t study finance, or haven’t quite grasped the financial jargons of business, sometimes in meetings, people throw out some technical finance terms and you find yourself nodding along but not quite sure about the technicalities. Today, we’re doing a simple crash course on “Net Present Value” (NPV).

Scroll down to see what it means, what it helps you figure out and how it works.

Let’s start simply. If you ask most people, they would say that the money you have in your account today is more valuable than the money you may have in the future. This is because you can use the present money to run a business, invest in something or even buy a Rolex and sell it for more in the future.

Future money is also less valuation due to inflation.

This very concept is called time value for money, but how do you properly compare the value of your money today vs. your money in the future. Ah, this is where the NPV comes in.

First off, let’s think about this. Would you prefer to have THB100 today or THB100 next year? Believe it or not, having THB100 today is worth more. Why? Simply because you have an opportunity to grow the THB100 today to be worth more by next year.

For example. Even if you deposit the THB100 in a bank, you’ll get an interest of THB0.5-THB1 by next year. It may be small, but you get the idea. Our take? Why not invest it?

Invest your money

Most of the time, unless something goes terribly wrong, the THB100 can grow significantly more than depositing it in a bank with 1% growth. Look into treasury bonds, corporate bonds, funds or even cryptocurrency.

As we have mentioned before in this content series, identify your risk appetite, research properly and only allocate what you can afford to lose.

For the sturdy and safe, say you buy a 20 year government bond today (yield is 2% per year). You will get almost 50% return in 20 years, so your THB100 will become THB150. You get the concept, right?

What is NPV, then?

“Net Present Value”(NPV) is a total of present value of cash flows over a period of time. In practical terms, it’s a method of calculating your return on investment (ROI). With NPV, you can typically look at the money you expect to make from that investment, and converting the returns into today’s baht or dollars. With this, you can then decide whether it’s worthwhile to invest.

Financial analysts often like to use NPV because ultimately, NPV answers a simple question: does the present value of all the money coming in over the span of the project outweigh how much money we have to spend in order to receive it?

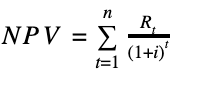

This is the NPV formula

As mentioned, getting 100 Baht today and in the next year are not the same because you can use 100 Baht today to generate more value within the next year. Therefore, if you get money later, we should discount this number with a “Discount rate”

The “Discount Rate”(i in the formula), or a rate of return you can make on an alternative investment. For example, you can invest in stock and get 5% return per year. A discount rate can also be company specific, or related to the cost of borrowing money.

- Lower discount rates =higher NPV (good).

- Higher discount rates=lower NPV (not so good).

The bottom line? Any investment that would generate a low or negative NPV should most likely be avoided.

An Example:

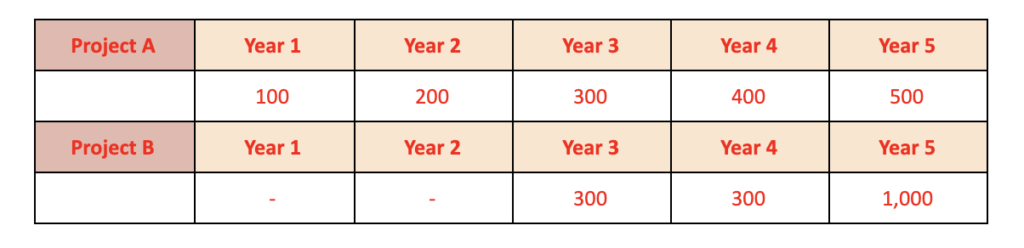

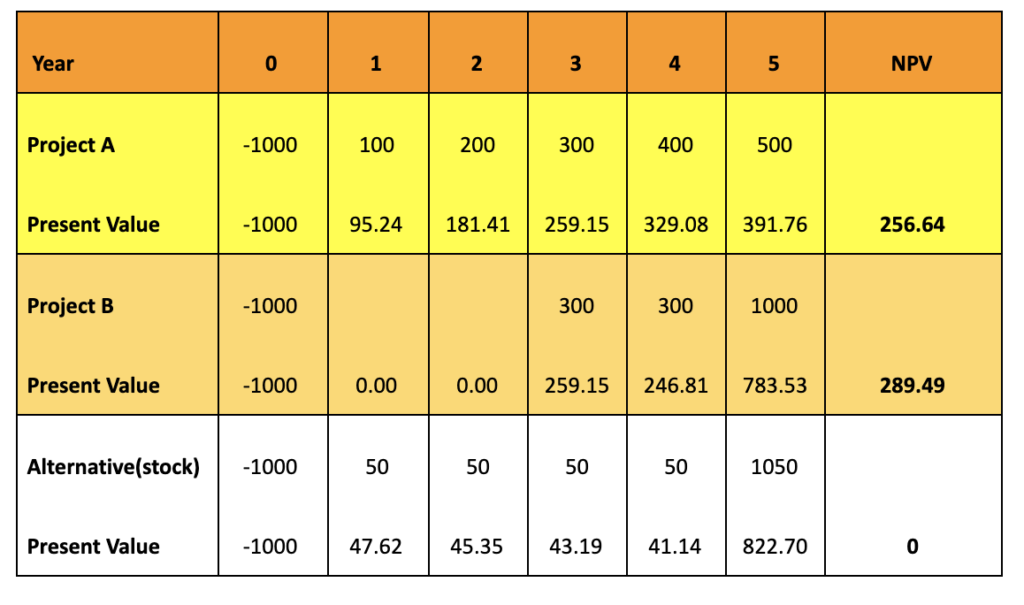

Bitesize is deciding whether to invest in Company A or Company B. Alternatively, we can also invest in the stock market which would generate a 5% return on investment.

For this example, the Discount Rate (i) is 5%.

Both companies will last 5 years with an investment cost of THB1,000.

Project A will generate a return of 100, 200, 300, 400, 500 Baht from year 1 to year 5

Project B will generate a return of 300, 300, 1000 in year 3,4, and 5.

Let’s use the table below for reference.

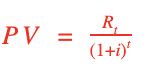

We can calculate “Present Value” (PV) using the formula below

- PV of project A in year 1 is 100/(1+0.05)1= 95.24.

- PV of Project B in year 5 is 1000/(1+0.05)5=783.53

- The sum of all present values is the “Net Present Value”

If we follow this logic, Bitesize should invest in Project B because NPV is greater than Project A and the alternative investment (stock market).

You know what though? For those who cannot form a formula off the top of their heads, you can simply open up an Excel spreadsheet and use the NPV function. If we follow this logic, Bitesize should invest in project B because NPV is greater than Project A and the alternative investment (stock market).

=NPV (discount rate, Value1, [Value2], [Value3],

Pro tip: Don’t forget to add in the “investment value” for year 0, which is always negative. In this case, it’s -1000.

What the NPV doesn’t show you

Granted, not all things are perfect, and neither is the NPV calculation. The calculation is based on educated assumptions and estimates, which means there are room for errors. For example, selecting the right discount rate is not all that easy.

The NPV also mainly deals with the cash flows of a project, and doesn’t include other critical costs. A higher NPV rate also doesn’t automatically translate to a successful investment, it also depends on the size and scale of the project.

With NPV, there is also the possibility that the investment will not have the same level of risk throughout its entire time period.

What this means is you should also not hesitate to adjust your initial numbers, and take in other considerations before taking the final plunge. Investments are typically more complex, and sometimes a simple spreadsheet doesn’t tell the whole story. Of course, it’s a good initial test.